Miscellaneous itemized deductions are those deductions that would have been subject to the 2 of adjusted gross income limitation.

Deductions not subject to 2 floor.

The regulations will apply to tax years beginning on or after may 9 2014.

This code has been deleted.

In prior years amounts subject to the 2 floor on line 13 of sch k 1 would have been coded with a k.

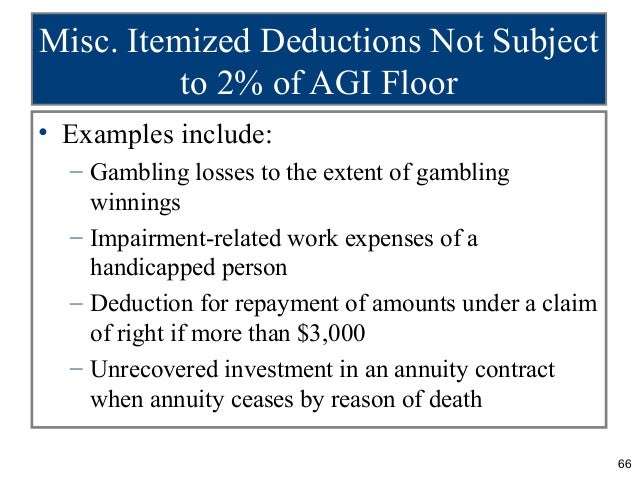

You cannot simply reduce your gambling winnings by your gambling losses and report the difference.

Miscellaneous itemized deductions subject to the 2 floor aren t deductible for tax years 2018 through 2025.

Examples of itemized deductions not subject to the 2 floor include costs related to fiduciary income tax returns and estate tax returns probate court costs and certain appraisal fees.

These porfolio deductions are not subject to the 2 floor.

1 deductions subject to the 2 limit these deductions allow you to deduct only the amount of expense that is over 2 of your adjusted gross income or agi.

Thus you should not need to make additional entries as other current year decreases.

However deductions under section 67 e 1 continue to be deductible if they are costs that are incurred in connection with the administration of an estate or a non grantor trust that would not have been incurred if the property were.

These losses are not subject to the 2 limit on miscellaneous itemized deductions.

To figure the amount of your allowable deduction for these expenses the irs provides a section on schedule a job expenses and certain miscellaneous deductions.

With respect to individuals section 67 disallows deductions for miscellaneous itemized deductions as defined in paragraph b of this section in computing taxable income i e so called below the line deductions to the extent that such otherwise allowable deductions do not exceed 2 percent of the individual s adjusted gross.

The irs issued final regulations on the controversial question of which costs incurred by trusts and estates are subject to the 2 floor on miscellaneous deductions under sec.

This publication covers the following topics.

For deductions that are subject to the 2 rule you may only deduct the part of the expenses that exceeds 2 of your adjusted gross income agi.

A type of expenses subject to the floor 1 in general.

Shall prescribe regulations which prohibit the indirect deduction through pass thru entities of amounts which are not allowable as a deduction if paid or incurred directly by an individual and which contain such reporting requirements as may be.

2 percent floor on miscellaneous itemized deductions.

2 percent floor on.

Deductions in excess of income in the final year of a trust or estate pass through to beneficiaries as miscellaneous itemized deductions even if the expenses.

You can still claim certain expenses as itemized deductions on schedule a form 1040 1040 sr or 1040 nr or as an adjustment to income on form 1040 or 1040 sr.